Introduction

In recent years, the obesity market has seen multifold growth thanks to the advent of new drugs and the widespread acceptance of their use in treating obesity. Obesity is a chronic condition linked to comorbidities like type 2 diabetes, cardiovascular disease, and certain cancers. Obesity has more than tripled over the past few decades, and it is estimated to affect more than 1 billion of the world’s population. This creates a market for the treatment and management of obesity. Currently, the obesity market is driven from the use of GLP-1 based drugs which have emerged to become mainstream making many analyst to project high growth margins of the market for the upcoming decade.

The market may continue to boom in the future as more effective drugs and innovative treatment methods are developed for obesity. Let’s take a closer look at recent trends and the competitive landscape in the obesity market.[1]

Recent Industry Trends

Recent trends in the obesity market show several transformative shifts:

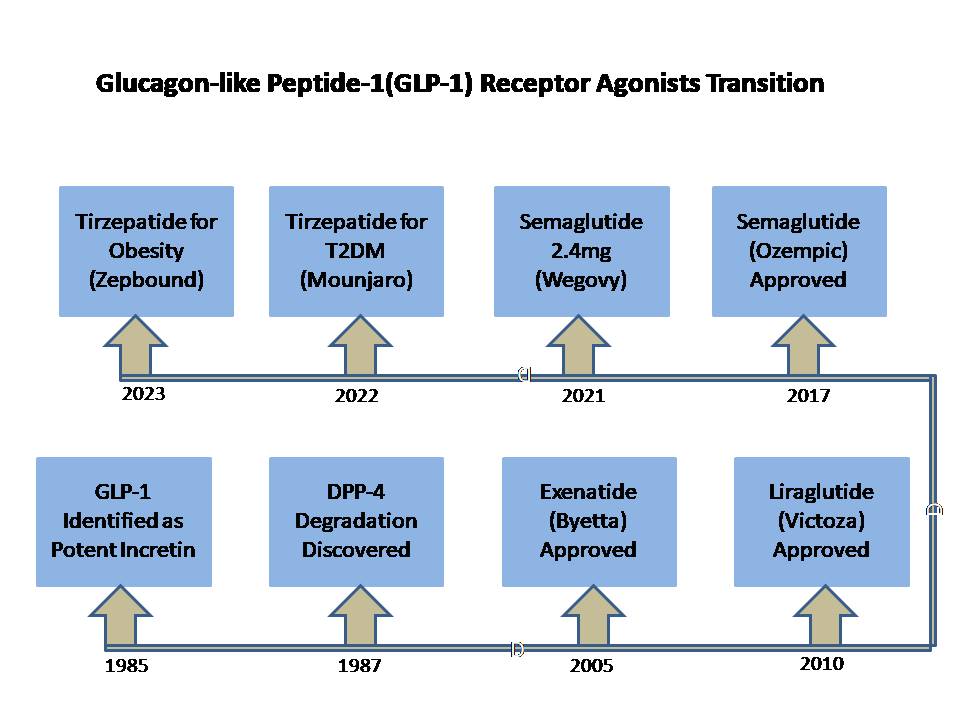

Pharmacological Innovation: The rapid rise of GLP-1 receptor agonist drugs, including well-known treatments like semaglutide and tirzepatide, has completely transformed the obesity treatment market in recent years. These medications were originally developed for diabetes, but clinical studies revealed that they can also produce substantial and sustained weight loss, making them highly valuable for obesity management. Their ability to reduce appetite, improve metabolism, and support long-term weight control has generated enormous interest among doctors, patients, and healthcare providers. As a result, demand has surged globally, leading to blockbuster sales, major pharmaceutical investments, and intense competition as companies race to develop next-generation therapies.[1]

Oral Treatment Expansion: Next-generation oral obesity therapies represent an important advancement in the treatment of obesity, as they offer a more convenient alternative to injectable medications. While current leading therapies, such as GLP-1 drugs, are often administered through weekly or daily injections, many patients prefer treatments that can be taken by mouth. As a result, pharmaceutical companies are investing heavily in the clinical development of oral weight-loss drugs that can deliver similar effectiveness with greater ease of use. These emerging therapies may improve patient adherence, expand access to obesity care, and attract a broader population seeking long-term weight management solutions beyond traditional injectable options.[2]

Partnerships & Licensing Deals: Major collaborations in the obesity market, such as AbbVie’s licensing agreements to develop new obesity treatments, reflect the growing industry-wide push to expand beyond current GLP-1-based drugs. While GLP-1 therapies have achieved remarkable success, pharmaceutical companies recognize the need for alternative approaches that may offer improved effectiveness, fewer side effects, or better long-term outcomes. Licensing deals and partnerships allow large companies to access innovative research from biotech firms and accelerate the development of therapies targeting different biological pathways. These collaborations highlight the competitive race to create next-generation obesity solutions and diversify treatment options for a wider range of patients.[3]

Emerging Market Focus: Companies in the obesity treatment industry are placing greater focus on emerging markets such as India and China, where obesity rates are rising rapidly due to urbanization, changing diets, and more sedentary lifestyles. These countries represent massive opportunities because they have large populations with growing healthcare needs, yet many patients remain underserved or untreated. To succeed in these regions, pharmaceutical firms are developing tailored market entry strategies, including affordable pricing models, local partnerships, expanded distribution networks, and regulatory adaptations. By targeting these untapped patient populations, companies can significantly increase their market reach, drive future revenue growth, and strengthen their global presence..[4]

Digital & Personalized Health:The integration of digital health technologies, remote monitoring tools, and personalized treatment plans is playing a major role in transforming obesity management. With the help of mobile health apps, wearable devices, and telemedicine platforms, patients can track their weight, physical activity, diet, and overall progress more effectively. Remote monitoring also allows healthcare providers to offer continuous support, adjust therapies in real time, and identify challenges early. Personalized treatment plans, tailored to an individual’s lifestyle, genetics, and medical conditions, improve adherence and long-term success. Together, these innovations enhance patient engagement, encourage healthier behaviors, and lead to better clinical outcomes in obesity care.[5]

Competitive Landscape

The obesity market is marked by intense competition among large pharmaceutical companies and specialized biotech firms:

Established Leaders: Major pharmaceutical companies such as Novo Nordisk and Eli Lilly have become the leading players in the global obesity therapeutics market, largely due to their success with GLP-1-based weight-loss drugs. These medications have shown strong clinical effectiveness, driving high demand worldwide and positioning these firms at the top of the competitive landscape. Together, they hold a significant share of the market’s total revenue, benefiting from blockbuster sales and widespread adoption among patients and healthcare providers. To meet rapidly growing demand, both companies have invested heavily in expanding manufacturing facilities, strengthening supply chains, and increasing production capacity for long-term market growth.

Emerging Competitors: In addition to major market leaders, several biotech firms and mid-sized pharmaceutical companies such as Amgen, Rhythm Pharmaceuticals, and AstraZeneca are actively developing innovative obesity treatments. These companies are focusing on new drug targets and alternative biological mechanisms beyond traditional GLP-1 therapies. Their goal is to create therapies that may offer improved weight-loss outcomes, fewer side effects, or better solutions for specific patient groups. Some of these treatments are designed for niche populations with rare genetic obesity disorders, while others aim for broader use in the general obesity market. This growing innovation increases competition and expands future treatment possibilities.

Generic/Biosimilar Entrants: As the patents on major obesity drugs, particularly blockbuster GLP-1 therapies like semaglutide and tirzepatide, begin to expire later in the decade, the market is expected to experience a significant shift. Once exclusivity ends, generic and biosimilar versions of these drugs can be manufactured and sold by other companies, often at much lower prices. This will introduce greater pricing competition, potentially making effective obesity treatments more affordable and accessible to a wider range of patients across different regions. Increased availability of lower-cost alternatives may also drive broader adoption, accelerate market growth, and reshape the competitive dynamics of the global obesity therapeutics sector.[6]

M&A Activity: The obesity therapeutics market has witnessed a surge in merger and acquisition (M&A) activity, particularly involving large pharmaceutical companies pursuing early-stage biotech innovators. These deals are often highly competitive, as major firms seek to acquire promising pipelines, novel drug candidates, or unique technologies before competitors do. Such strategic moves allow big pharma to secure long-term growth in a rapidly expanding and high-potential market, while diversifying their portfolios beyond existing products. By investing in innovative therapies at an early stage, companies can gain a competitive edge, accelerate development timelines, and position themselves as leaders in the evolving obesity treatment landscape.[7]

Relevant Patents and Their Timeline

Intellectual property protection plays a crucial role in shaping competition and market dynamics of the obesity market through various patents:

Semaglutide (e.g., Wegovy/Ozempic): The patents protecting the chemical compositions and formulations of semaglutide, a leading GLP-1-based obesity and diabetes drug, are set to expire in major global markets around 2031. Once these patents lapse, other pharmaceutical companies will have the legal opportunity to produce biosimilar versions of semaglutide, which are highly similar in efficacy and safety but generally offered at lower costs.

Tirzepatide: Tirzepatide, a newer and highly effective obesity and diabetes medication, benefits from patent protection that extends significantly longer than some other drugs in the market, potentially until 2036. This extended patent life provides the current developers with a prolonged period of market exclusivity, during which they can exclusively manufacture and sell the drug without direct competition from generics or biosimilars. The longer exclusivity window allows the company to maximize revenue, recoup research and development investments, and strengthen its position in the obesity therapeutics market. It also gives them strategic flexibility to expand indications, optimize formulations, and solidify their global market share before patent expiry.

Next-Gen Therapies: In recent years, there has been a significant increase in the filing of patents for next-generation obesity therapies, including innovative approaches like dual-agonist drugs and oral weight-loss compounds. Dual-agonists target multiple biological pathways simultaneously, potentially offering greater efficacy than single-target treatments, while oral formulations provide improved convenience and patient adherence compared to injections. These patents are being filed globally, highlighting the strategic focus of pharmaceutical and biotech companies on developing breakthrough solutions that can redefine obesity treatment. As these drugs advance through clinical trials and regulatory approvals, the associated patents will play a critical role in determining market exclusivity, competitive positioning, and long-term profitability.

Revenue Projections

Market forecasts illustrate strong growth potential for the obesity treatment sector:

- Global Market Growth: The global obesity treatment market was valued at around USD 15.9 billion in 2024 and is projected to reach USD 60.5 billion by 2030, expanding at a compound annual growth rate (CAGR) exceeding 20%.

- Regional Expansion: The U.S. market is expected to grow sharply as well—one estimate projects revenue to increase from around USD 11.2 billion in 2024 to nearly USD 48.5 billion by 2030.

- Longer-Term Outlook: Other forecasts suggest broader growth into the mid-2030s, with some scenarios estimating total obesity treatment market revenues could rise significantly as oral therapies, personalized care solutions, and global access expand.[8]

Overall, the projected growth reflects not only the rising prevalence of obesity but also increased investment, wider treatment availability, and diversification of therapeutic approaches.

Conclusion

The obesity market is undergoing rapid transformation, driven by strong epidemiological demand, innovative pharmacological developments, and dynamic competition between established pharmaceutical leaders and emerging biotech players. With blockbuster therapies reshaping treatment paradigms, expanding global access, and evolving patent landscapes, the industry is poised for substantial revenue growth through the 2030s. However, emerging competition, pricing pressures, and regulatory complexities will also influence how opportunities unfold in this high-growth healthcare segment. Careful monitoring of patent expirations, competitive moves, and clinical innovations will be key for stakeholders seeking strategic positioning in the evolving obesity market.